Global Dairy Market Outlook 2024

Global dairy market: Price recovery will be slower than expected, but the outlook remains positive

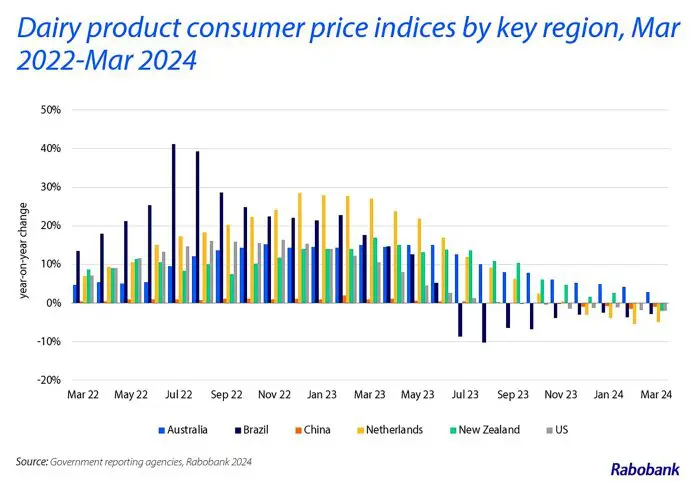

A recent Rabobank report indicates that the initial surge in dairy prices seen in late 2023 and early 2024 was largely due to a period of restocking at lower prices rather than a robust uptick in consumer demand. The report suggests that the global dairy market may experience a slower price recovery than previously anticipated, particularly as China shows a reduced need for dairy imports. Despite this, the overall market outlook remains positive.

Milk prices and supply face challenges amid modest demand

The recovery in global milk prices has encountered some headwinds in Q2 2024. Earlier expectations of gradual price increases throughout the year have been tempered by a combination of weaker global demand and increased domestic milk production in China, which has led to a reduction in imports. These factors suggest that dairy prices may encounter further obstacles on the path to recovery.

While China has seen an upward revision in its milk production forecast for 2024, other key dairy-producing regions are not faring as well. The US and South America have experienced a reduction in dairy herds due to low profitability, and adverse weather conditions have impacted milk output in New Zealand and Europe.

Subdued consumer sentiment and recent buyer caution dampen demand

“Mixed signals in demand recovery are emerging, and consumers’ purchasing power remains under pressure. While unemployment remains close to record lows in most large markets, consumer sentiment is gloomier than anticipated. Inflation remains above target in most countries, and high interest rates continue to pressure debts and consumer spending at a time when credit plays an important role after cumulative inflation in recent years,” explains Andrés Padilla, Senior Dairy Analyst at Rabobank. In China, a weak job market and low consumer confidence have led to a more restrained consumption pattern, despite a temporary boost during the Lunar New Year.

Moreover, dairy buyers who previously capitalized on lower prices to restock are now approaching the market with more caution. The anticipation of a seasonal increase in milk production from the Northern Hemisphere has led to a more measured pace of purchasing at current price levels.

Cheese and butter exports flourish, while skim milk powder dwindles on the back of reduced Chinese imports

Compared to the previous year, China’s net dairy imports are forecast to drop by 8% in 2024. A combination of increased domestic production and faltering demand is expected to reduce China’s dairy deficit, with significant declines in skim milk powder imports in particular.

In contrast, demand for cheese and butter remains robust and is predicted to continue outperforming in most regions. These products are expected to sustain their export momentum, even as the market adjusts to shifting demand patterns.

Lower feed costs bolster farmer margins

On a more encouraging note, dairy farmers can expect some relief. Feed costs have come down, and farmgate milk prices have responded by moving higher since late 2023, in line with the increase in commodity prices. “Affordable prices for key commodities like soybeans and corn are projected to remain stable or decrease in the second half of 2024,” says Padilla. “Even if global prices remain relatively stable for some months, higher farmer margins should spur some production growth later in 2024.”

More information

Please contact the report’s author:

Andrés Padilla, andres.padilla@rabobank.com, +55 (11) 55036936

Further information:

Rabobank press office, pressoffice@rabobank.nl, +31 30 216 2758

June 2024

Article and Photo courtesy of Rabobank

For Leading Industry News in the Cattle Field: Home – American Cattlemen